The securities finance industry is currently digesting the heavy meal that has been Basel III, CRD-IV, Dodd-Frank and related regional regulatory initiatives impacting the global market. These are not light appetizers at all. Rather, financial intermediaries are facing tough questions about how they will move forward in their business models. This article looks at the three main options facing market participants in their business decision making, some negative and some positive, and offers SunGard findings on market trends.

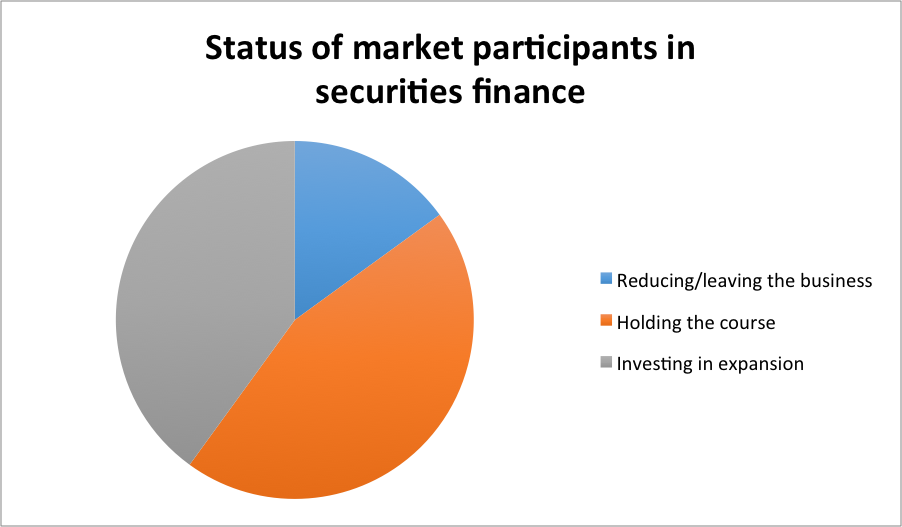

SunGard has identified three strategies that financial intermediaries are considering in 2015. The ‘Get Out Now’ strategy involves leaving the market, or at least reducing a firm’s market footprint to conduct the minimum amount of business necessary for basic financing maintenance. The ‘Wait and See’ strategy is what it sounds like: hold the current course, focusing on efficiencies until more is known about the market in two to three years. The ‘Double Down’ strategy looks at opportunities in the securities finance space across products to take advantage of areas where competitors are stepping back. SunGard finds that 15% of participants are planning to reduce their footprint or leave the market, 45% are holding on for better times, and 40% are making investments or evaluating costs in preparation for growth. These firms are found across all tiers of intermediaries, including the largest banks.

Source: SunGard’s Apex Securities Finance

The Get Out Now Strategy

Leaving any marketplace is a difficult decision, taken only after substantial soul searching. Leaving securities lending or repo is even more difficult given the fundamental impacts that these businesses have on financial intermediary business lines. Leaving securities lending may mean a loss of inventory for prime brokerage clients, or exiting a matched book program. Exiting repo could impact government bond trading at a basic level. Taken as standalone businesses, securities finance may look unattractive, but their roles as the lubrication of financial markets is well known. But this is the decision that some firms have come to or are actively considering.

The rationale for exiting the market is driven by regulation that has made spreads, factored after internal liquidity or collateral costs, untenable. The Liquidity Coverage Ratio, coupled with a lack of counterparty interest in accepting equities as collateral, may create inflow and outflow ratios that do not add up to firm-wide requirements. It is possible that this same business could be conducted on a central counterparty (CCP) and avoid the worst of capital requirements, but that is still a hypothesis. In the meanwhile, capital costs are a reality and returns on securities lending transactions are unproven and may not hold up in the new frontier of securities finance.

In repo, the Leverage Ratio has already pushed government bond repo to unusual spreads at quarter end. In the U.S., spreads on March 31, 2015 ranged from 6 bps (offered by dealers to clients) and 125 bps (bid by dealers from clients). As financial intermediaries need to report their figures and require a best possible Leverage Ratio, repo is a logical target. Again, CCPs may solve some of the problem but not all, given that CCPs add their own costs and potential complexities to the market. Is it any wonder that a financial intermediary may choose to exit the market?

The down side of the ‘Get Out Now’ strategy is a great loss of capability. The need to go through another financial intermediary to access the same service that was just lost only adds costs to clients. But what’s worse, absorbing the cost internally or paying more for each incremental transaction? It may be that the latter is the worse option.

The Wait and See Strategy

The ‘Wait and See’ crowd may have the right idea: do nothing for now and see how the market develops. This group needs to be and must remain in securities finance for client purposes, otherwise they may join the ‘Get Out Now’ firms. Although costs are increasing, these firms know that they can pass on costs to clients when needed and can seek cost-effective alternatives where possible, often looking at cost efficiencies in technology and business processing outsourcing. SunGard is at the forefront of the evolution, working with their clients to provide partnership services in solutions. These firms are typically balancing multiple product lines including synthetic prime brokerage and futures as well. In response, SunGard has launched Apex Securities Finance 2015 to enable firms to undertake their securities finance activities efficiently and within the changing regulatory environment.

The Double Down Strategy

The ‘Double Down’ group is the most dynamic in securities finance these days. They recognize that securities lending or repo may be difficult, but the economic need for similar transactions stay the same. This is the group that is most actively looking at Contracts for Differences, Single Stock Futures and other potentially cleared transactions as an alternative to securities loans. They are also energized by equity swaps and Delta One business whether bilateral or cleared. Everything has a price including balance sheet utilization, providing the motivation for these firms, and why they are working with their clients to find the best way forward.

The ‘Double Down’ group is the most exciting to watch and with good reason. These firms are typically first to join new CCPs and other market initiatives; they have less to lose than their competitors in trying new routes to market. They are also looking at cost rationalizing with the goal of preserving and growing their market while competitors pull back. These firms are also looking at various combinations of outsourcing and reorganizations to keep their franchises healthy.

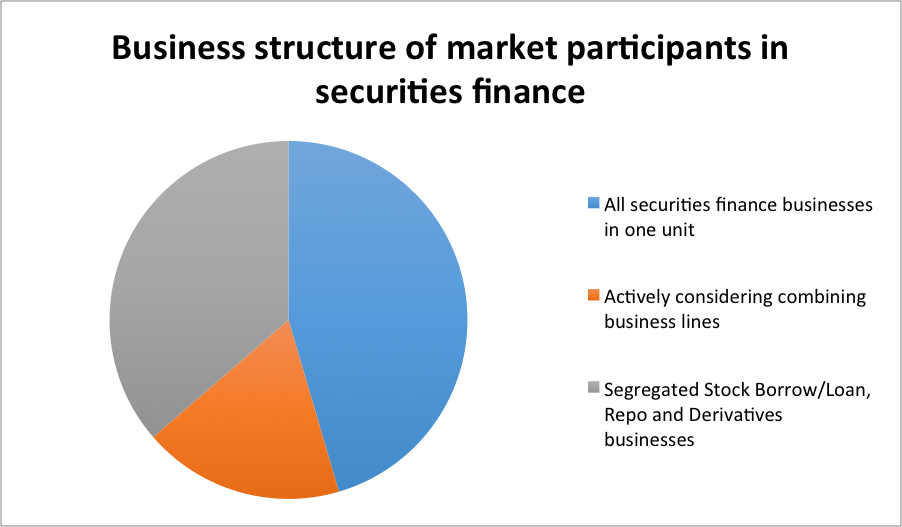

One option considered lately is merging securities lending and repo into one business unit. It remains a confusing state of affairs that there are two historically distinct business lines that serve an overlapping economic purpose. What makes an equity repo substantially different than an equity securities loan vs. cash? Not much. The trouble is when two business units are trading these products, there is no one CCP or necessarily a Master Netting Agreement that can cover both. Merging business units should result in one product taking over more volume with concomitant benefits to firm balance sheets. In addition, firms can benefit from combined technology platforms and solutions, continuing the focus on driving down costs.

SunGard recently investigated the idea of merging securities lending and repo desks, and found that approximately 50% of our current clients were already running repo and stock borrow/loan/securities lending under one organizational unit. Another 20% were actively considering merging business lines, while 30% are keeping their lending, repo and derivatives businesses separate.

Source: SunGard’s Apex Securities Finance

Options for Staying in the Market

There is no question that now is a difficult time to be in securities finance. Change is hard in any circumstance; it is harder now with the phenomenal quantity of regulatory risk reduction that has entered the market. Like any transition, it can be expected that there will be a shakeout, then market participants will find routes and operational processes that lead to greater profitability. At SunGard we see several options that may assist financial intermediaries in managing the transition:

- Industry utilities. SunGard has been working to reduce market participant cost through the launch of industry utilities for derivatives clearing and securities lending processing. We recognize that our clients have substantial fixed costs; transactions processing does not need to be one of them. A move towards outsourcing securities finance operations can reduce total cost of ownership while keeping intact the software and services that clients need.

- Product consolidation. SunGard recognizes that our clients businesses are changing, and we are changing with them. We are merging, consolidating and adapting our solutions to suit the business and operational requirements of clients in securities finance as they adapt their own models. We expect to continue this process to help clients manage their transitions to the post Basel III-regime as best as possible. The Apex Securities Finance 2015 solution combines these multiple business lines and cross product requirements to provide a consolidated platform for the overall securities finance front office and operational needs.

Securities finance has a long life ahead of it; of that we are certain. However, the traditional bilateral securities lending and repo businesses may not be the way forward. Financial intermediaries must adapt to new pressures in order to sustain their businesses. While some firms will choose to exit the market, others will wait to see what comes next or are investing in their securities finance franchises for greater growth. The next three years will see continued change in the securities finance marketplace; how financial intermediaries act now will determine their future standings in this evolving space. SunGard will continue to build strategic partnerships as clients evolve within the marketplace to ensure it provides leading services and solutions for the securities finance landscape.

Tom Dibble is Head of Product Management at SunGard’s Apex Securities Finance